Feeling overwhelmed and hopeless due to debt is a common experience. However, by implementing strategic planning and discipline, individuals can liberate themselves from the burden of debt and achieve financial freedom. This journey requires confronting your finances head-on, understanding all your options, and sticking to a tailored debt relief plan.

Follow these 10 essential steps to effectively manage debt, improve your credit score, and pave the way to financial freedom.

The Psychological Toll of Debt

Becoming trapped in debt often exerts immense psychological pressure, posing barriers on the path to financial freedom. Feelings of shame, anxiety, stress, and hopelessness are common when facing unmanageable debt. Debt strains relationships with loved ones too. However, understanding these typical responses and finding healthy coping methods helps overcome the emotional toll.

According to the National Library of Medicine, over 75% of people with debt report moderate to high levels of anxiety tied directly to their financial obligations. Employing stress management skills like meditation and exercise helps mitigate anxiety and despair when debts feel overwhelming. Seeking mental health support also aids in managing any severe depression symptoms stemming from debt.

While the emotional impacts are challenging, hope should not be lost. The psychological toll of debt is temporary. With time, effort, and a debt relief plan, the satisfaction of becoming debt-free will eclipse past struggles. Equipped with this emotional resilience, you can now confidently explore the key practical strategies to regain financial freedom.

10 Key Steps to Financial Freedom

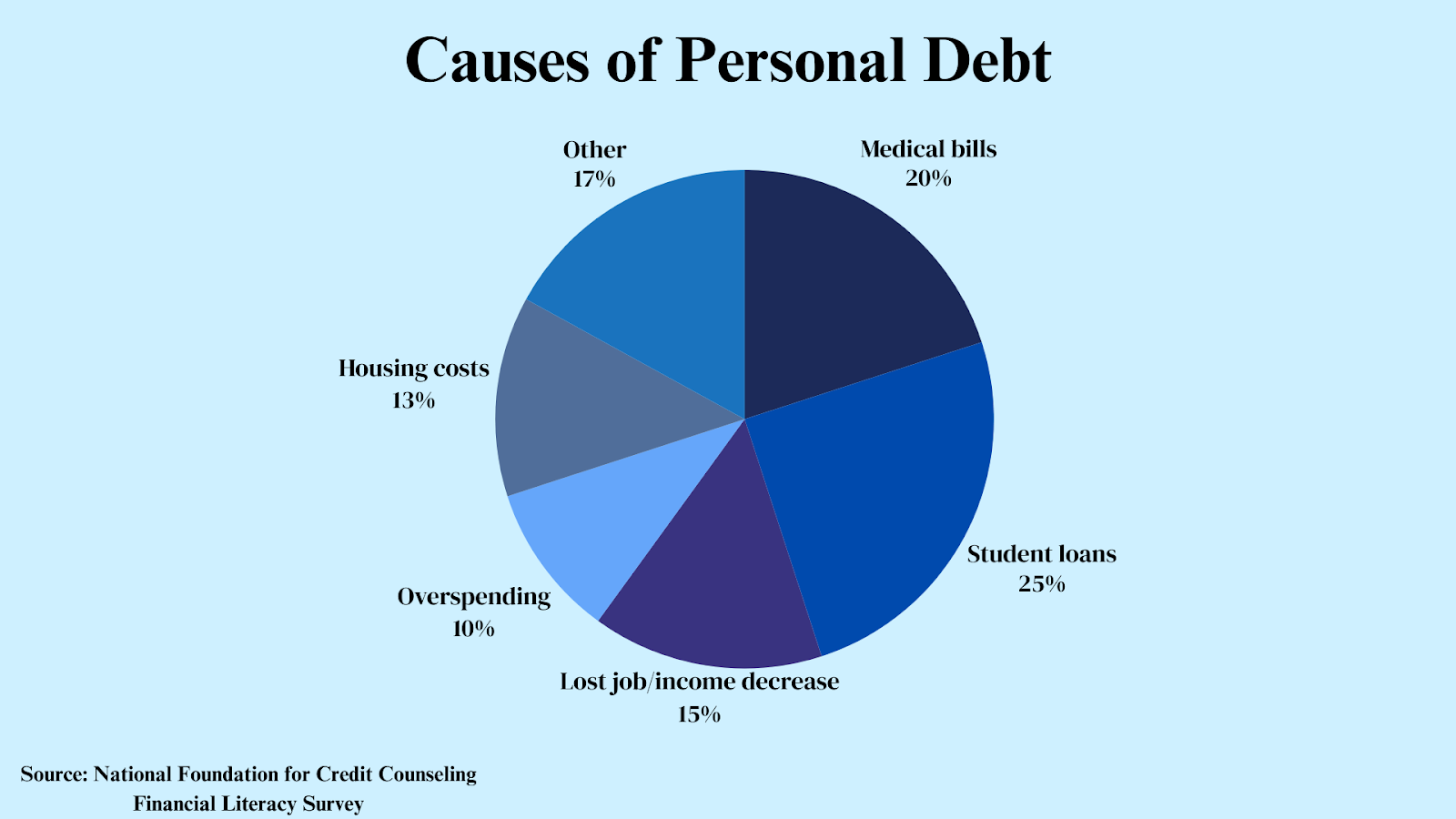

I. Acknowledge the Full Extent of Your Debt

The first step to gaining control of your financial life is confronting your debt head-on. First, you need to understand what causes personal debt. Look at the data below that shows the common reasons for personal debt:

Next, start by compiling a comprehensive list of all debts you currently owe, including your other debts like payday loans or tax debts. For each debt, note key details like the remaining balance, interest rate, minimum payment, and loan term.

Prioritize listing high-interest debts first, as these accrue the most in interest fees and should be targeted for repayment urgently. List subsidized and unsubsidized student loans separately, as their terms differ. Account for all mortgages and home equity loans secured against your property. Detailed medical debts owed to various providers and relevant interest rates if applicable.

Evaluating the complete picture of all debts owed, from various sources, helps you grasp the cumulative impact on your net income and credit score. This perspective enables you to identify priority debts for repayment and opportunities to consolidate or refinance at better rates.

Do not disregard any obligations simply because payments are not currently due or interest rates seem low. Completely acknowledging the reality of total debts owed is essential to take control of your finances and begin eliminating debt.

II. Create a Comprehensive Budget

With the average debt burden around $45,300 for recent bachelor’s degree holders, budgeting is critical for managing debt repayment. Analyze your income, organizing essential and discretionary expenses. Look for areas to reduce spending on wants rather than needs. Account for all foreseeable costs in your budget, while allocating as much excess income as possible towards debt repayment.

With all debts clearly documented, the next step is creating a comprehensive budget accounting for your full financial picture, including:

- Track income – Note all sources of income, including wages, side hustles, gifts, and other inflows. Calculate take-home pay after taxes.

- List fixed expenses – Housing, utilities, transportation, insurance, minimum debt payments, and other set costs.

- Estimate variable expenses – Groceries, dining out, entertainment, clothing, etc. Based on actual past spending.

- Identify discretionary expenses – Wants like vacations, hobbies, and other non-essential costs. Distinguish needs from desires.

- Account for irregular expenses – Annual fees, car registration, medical costs, home repairs. Plan for infrequent bills.

- Allow for emergency savings – Consistently allocate funds to build your safety net over time.

- Prioritize retirement savings – Contribute to retirement accounts, balancing present and future.

- Maximize debt payments – After essentials, allocate as much excess income as possible to debt repayment.

- Re-evaluate and adjust – Review your budget periodically and adapt spending as circumstances change.

A realistic budget aligned with your values visualizes your cash flow, empowering you to meet obligations while still preparing for the unexpected. Sticking to your budget while maximizing debt payments creates a path to financial freedom.

III. Explore Debt Relief Options

A range of debt relief options exist to help manage unaffordable debts. Federal student loan forgiveness programs, including income-driven repayment plans and public service loan forgiveness, offer options to discharge student loans after an extended repayment period. The current administration also has broad student debt cancellation initiatives pending, subject to borrower qualifications.

Mortgage refinancing at a lower interest rate can reduce monthly payments without extending the loan duration, although closing costs may apply. Non-profit credit counseling services provide debt management plans that consolidate debts into one payment and negotiate reduced interest rates or waived fees on your behalf.

More drastic options like debt settlement through lump-sum payouts, debt consolidation loans, and bankruptcy carry greater credit score risks but can provide relief in dire circumstances.

Those in Michigan can also explore reputable local Michigan debt relief consultation services. Choosing the right debt relief solution depends on your specific circumstances and goals. Carefully evaluating all choices allows you to identify the most effective option to regain control of your finances.

IV. Establish an Emergency Fund

As life inevitably brings financial surprises, an emergency fund provides a vital insurance policy enabling you to respond without sinking deeper into debt. Begin building emergency savings with these steps:

- Set a savings goal – Experts recommend a starter emergency fund of $500 to $1,000 and an ultimate goal of 3-6 months’ worth of essential living expenses.

- Find the money – Allocate a fixed amount from your monthly income before spending on non-essentials. Consistency is key, even starting with small deposits.

- Select a secure account – Opt for an easily accessible savings or money market account. Compare interest rates and choose the highest yield within your risk tolerance.

- Make regular contributions – Automate transfers from checking to savings each month. Even small amounts contribute to growth over time thanks to compound interest.

- Limit withdrawals – Only tap emergency funds for true necessities like job loss, illness, or major car repair. Keep the account impact minimal and focused.

Replenish any withdrawals quickly to restore savings safety net. With an established emergency fund, unexpected expenses do not have to mean accumulating additional debt.

V. Negotiate with Creditors

Negotiating directly with creditors can provide critical debt relief, especially when paired with larger-scale debt forgiveness initiatives. When you simply cannot afford monthly payments, proactively reaching out to request alternate repayment terms can make debts manageable once again.

Contact lenders directly through phone, email, or certified mail. Clearly explain your financial hardship and inability to maintain existing required payments. Provide evidence of income and expenses if required. Then make a specific request for reduced interest rates, waived fees, lowered minimum payments, or other flexible options.

Remain polite but firm in negotiations. Highlight how alternate arrangements allow you to continue making regular payments and avoid default or bankruptcy, which creditors want to avoid. Consider including goodwill gestures like making a partial lump-sum payment upfront if you have some available funds.

Document all negotiations and agreed terms in writing for accountability. Follow-up discussions in writing to confirm details. While positive negotiation outcomes depend on each creditor’s policies, being proactive maximizes the chance of success. If initial requests are denied, persistently appeal or offer alternatives.

If negotiations fail and debt becomes unmanageable again, promptly pursue other relief options before defaulting. This protects your creditworthiness and future options.

| Negotiation Strategy | When It Works Best |

| Lower Interest Rate | If the rate is very high compared to current market rates |

| Waived Fees | If fees are excessive and can be reduced or removed |

| Lower Minimum Payment | If payment is truly unaffordable based on income |

| Extended Loan Term | If the term can be lengthened to reduce monthly dues |

| Offer a Lump Sum | If you have access to a portion of the balance |

Staying engaged with creditors, documenting all arrangements, and providing evidence of true financial need gives negotiations the best chance of success. Relief depends on each creditor, but perseverant efforts optimize potential win-win solutions.

VI. Consider Professional Debt Relief Services

If you feel overwhelmed tackling debt independently, consult reputable credit counseling agencies or debt management services. Research thoroughly and avoid scams, but such support can facilitate consolidating debts into one personalized payment plan and negotiating with creditors on your behalf.

Weigh the value of these services against their costs to determine if they’re beneficial for your circumstances. Their expertise can be invaluable for negotiating debt relief, but their advice may also help you self-manage debts.

VII. Prioritize High-Interest Debt First

To optimize savings, employ the debt avalanche method – focusing on the highest-interest debt first while making minimum payments on all other debts. List debts by interest rate, dedicating all extra repayments to the most expensive debt. Once that’s paid off, roll that amount to the next highest-interest debt, snowballing funds toward the next priorities.

This strategic approach saves significantly on interest costs compared to paying off lower-rate debts first or spreading repayments evenly. Stick to this efficient repayment hierarchy, adjusting as interest rates change over time.

VIII. Increase Your Income

While cutting excess expenses is wise, maximizing income accelerates debt repayment. Explore side hustles or freelancing utilizing your talents and skills. Sell unused possessions through online platforms. Ask your employer for a raise if you’ve increased your responsibilities. Every extra dollar should fund debt payments in priority order, driving progress each month.

Additional income streams also help build savings and provide financial breathing room. But focus this supplemental income on freeing yourself from debt first before increasing lifestyle spending.

IX. Monitor Your Credit Score

As you make debt relief strides such as through World Bank and government-backed programs, keep tabs on your credit reports and scores. The progress you’re making may not always be immediately reflected. Ensure no errors or unfamiliar accounts appear that could wrongly penalize your creditworthiness as debts decrease.

Your income-to-debt ratio and credit mix also influence scores. So while debts shrink, also focus on responsibly increasing available credit through strategic account opening, loans, or secured cards to demonstrate fiscal health.

X. Stay Committed to a Debt-Free Lifestyle

Shedding debt requires diligence and devotion, but with each milestone, your motivational momentum builds. Remain focused on the financial, psychological, and social benefits you’ll gain without the debt burden. Surround yourself with a support system that shares your debt-free vision to stay the course when challenges arise.

Let go of feelings of failure and focus on the wins. Celebrate your discipline as debts decrease, visualizing and achieving a life liberated from debt. Your commitment will be richly rewarded.

Conclusion

The road to financial freedom via debt relief can be arduous, but incredibly worthwhile, step-by-step. Confronting what you owe, budgeting wisely, utilizing all options available, increasing income, monitoring your credit, and visualizing your debt-free future will empower your success. You have the power to take control of your debt situation and build the financially liberated life you desire and deserve.

Frequently Asked Questions on Debt Relief Essentials

1. What are the first steps to achieving financial freedom from debt?

Start by acknowledging the full extent of your debt, including all loans, credit cards, and mortgages. Then, create a comprehensive budget to manage your finances effectively.

2. How important is creating a budget in debt relief?

Creating a budget is crucial as it helps you track your income, and expenses, and allocate funds towards debt repayment efficiently, ensuring you can manage your debts without compromising your daily needs.

3. What role does an emergency fund play in debt relief?

An emergency fund acts as a financial safety net that prevents you from taking on more debt in case of unexpected expenses, ensuring that your debt relief efforts are not derailed.

4. Can negotiating with creditors really help reduce my debt?

Yes, negotiating with creditors can lead to lower interest rates, waived fees, or a more manageable repayment plan, which can significantly reduce your overall debt burden.

5. Are debt consolidation loans a good idea?

Debt consolidation can be beneficial if it results in a lower overall interest rate and simplifies your payments, but it’s important to consider the terms and potential impact on your credit score.

6. How do debt relief programs work, and are they worth it?

Debt relief programs, such as debt management or settlement, can help reduce your debt load or lower your monthly payments. However, it’s vital to research and consider any potential fees or impacts on your credit score.

7. What’s the difference between the debt snowball and avalanche methods?

The debt snowball method involves paying off debts from smallest to largest to gain momentum, while the avalanche method focuses on paying down debts with the highest interest rates first, potentially saving more money in the long run.

8. How can increasing my income aid in debt relief?

Increasing your income through side gigs or other means can provide extra funds to allocate towards debt repayment, accelerating your progress towards financial freedom.

9. Why is monitoring my credit score important during debt relief efforts?

Monitoring your credit score is essential to understand the impact of your debt relief efforts, identify any errors, and track your progress towards improving your financial health.

10. What strategies can help me maintain a debt-free lifestyle once I’ve achieved it?

Living within your means, continuing to budget, saving for emergencies, and avoiding unnecessary credit use are key strategies for maintaining a debt-free lifestyle.

11. How does student loan debt affect financial freedom, and what relief options are available?

Student loan debt can significantly impact financial freedom due to its size and repayment terms. Relief options include income-driven repayment plans, loan forgiveness programs for certain professions, and potentially refinancing to lower interest rates.

12. How do I decide if bankruptcy is the right option for debt relief?

Bankruptcy should be considered a last resort due to its long-term impact on your credit score and financial health. It’s best to consult with a financial advisor or bankruptcy attorney to explore all other debt-relief options and understand the consequences before proceeding.

13. Can debt relief affect my credit score?

Yes, certain debt relief actions, like debt settlement or filing for bankruptcy, can negatively impact your credit score. However, consolidating debts or entering a debt management plan may have a less detrimental effect and can eventually lead to an improved credit score as debts are paid off.

14. Are there any risks associated with debt relief services?

While debt relief services can offer a path to financial freedom, there are risks, such as potential scams, fees, and the impact on your credit score. It’s crucial to research and choose reputable services and fully understand the terms and conditions before committing.

15. How can I protect myself from debt relief scams?

To protect yourself from scams, look for accredited debt relief services with positive reviews and transparent fee structures. Be wary of companies that promise quick fixes, charge upfront fees before providing any services, or ask you to stop communicating with your creditors. Always verify the credibility of the service through trusted consumer protection sites like the Better Business Bureau or the Consumer Financial Protection Bureau.

Leave A Comment